(858) 863-0261

connect@greenmeansgrow.com

I Want In [Buy]

I Want Out [Sell]

Sell

Get A Cash Offer

I Want Money [Borrow]

Free Home Evaluation

Meet The GreenTeam

More

Trending Now

Social Wall

Contact

I Want In [Buy]

I Want Out [Sell]

Sell

Get A Cash Offer

I Want Money [Borrow]

Free Home Evaluation

Meet The GreenTeam

More

Trending Now

Social Wall

Contact

I Want In [Buy]

I Want Out [Sell]

Sell

Get A Cash Offer

I Want Money [Borrow]

Free Home Evaluation

Meet The GreenTeam

More

Trending Now

Social Wall

Contact

Types of Mortgages

Low Interest Rates won’t last Forever, Act Now!

February 23, 2021

...

Read More

Don’t Fit In The Conventional Lending Box? We Got You Covered

December 4, 2017

...

Read More

Why It Takes Years To Save For A Down Payment

January 30, 2017

...

Read More

Mortgage Pre Qual vs. Pre Approval

August 22, 2016

...

Read More

The Subprime Mortgage Meltdown….explained by stick figures!

August 15, 2016

...

Read More

Is This Your Best Chance Yet To Buy A Home?

August 8, 2016

...

Read More

3 Ways To Access Your Home’s Equity

May 16, 2016

...

Read More

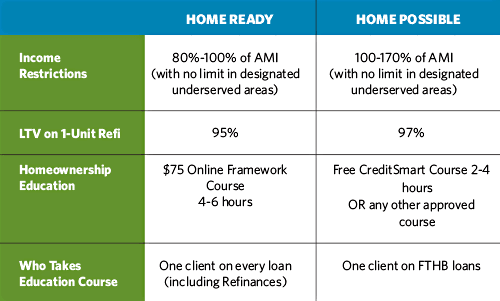

2 Loan Programs You Must Know About

March 28, 2016

...

Read More

Two Home Loans You Must Consider

May 29, 2015

...

Read More

The One Thing All Self Employed People Need to Know

May 4, 2015

...

Read More

Show more